Many traders use technical and/or fundamental data, but few traders have discovered the unique benefits of using sentiment data in their investment process. Sentiment data attempts to quantify the emotional mood of investors and traders and can be used as a very effective contra-indicator. When traders are complacent and overly bullish, markets tend to pull back. Conversely, when traders panic and emotions are running high, this often indicates a potential bottom and an attractive buying opportunity. The following article presents a unique and troubling sentiment warning signal from a recent proprietary research report from SentimenTrader.

SentimenTrader Research Study

I have a paid subscription to SentimenTrader, which supplies data that I use in several of my algorithmic trading strategies, but I am not otherwise affiliated with SentimenTrader. Last week, SentimenTrader published an interesting proprietary research study that they have allowed me to share on Trader Edge. It is a representative example of how to use market sentiment and it generated a unique warning signal that is not reflected in other data.

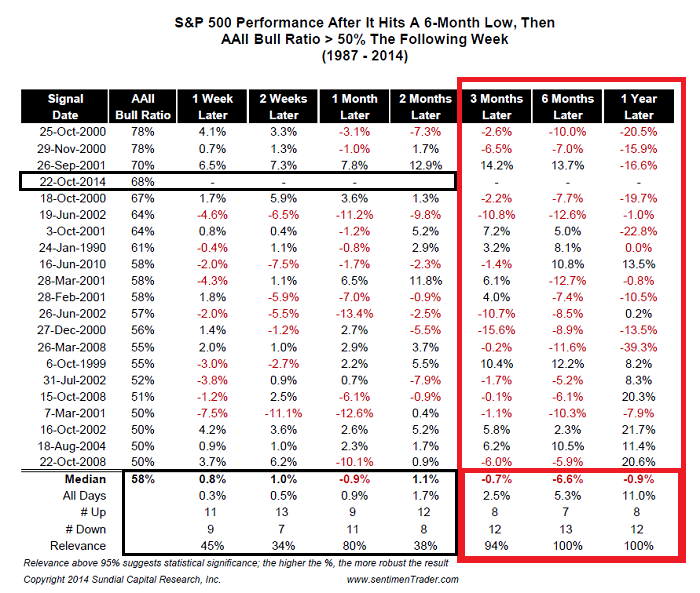

The table in Figure 1 below documents the performance of the S&P 500 index when the index records a 6-month low and the American Association of Individual Investors (AAII) Bull Ratio exceeds 50% the following week. The data from the table covers the period from 1987 through the present.

Normally, when the S&P 500 pulls back to a 6-month low, investors would have begun to panic and head for the exits, especially when bombarded by a steady stream of bad news:

- the end of QE

- the prospect of the Fed increasing short-term interest rates in 2015

- the eventual liquidation of the unprecedented Fed balance sheet

- evidence of economic weakness in Japan, Europe, and China,

- the startling rise of ISIS (including public beheadings),

- renewed Russian aggression and expansion in Ukraine, and

- the rapid spread of Ebola with unknown economic consequences

Following a 6-month low in such an environment, market sentiment would normally be extremely negative. Instead, on 10-22-2014 the AAII Bull Ratio was a euphoric 68%. Granted, the market did rally after dropping to a six-month low, but this is a highly unusual and overly complacent sentiment reading. In the week following a 6-month low in the S&P 500 index, the AAII Bull Ratio has only exceeded 50% twenty times since 1987. The 68% reading on 10-22-2014 was the fourth highest during this period.

In that context, let's look at the table in Figure 1 below. The date of the signal and the AAII Bull Ratio are presented in the first two columns at the left-side of the table. The next seven columns provide the returns of the S&P 500 index over the subsequent 1 Week, 2 Weeks, 1 Month, 2 Months, 3 Months, 6 Months, and 1 Year. The data are provided for all 20 historical observations.

Summary information is provided at the bottom of the table for each of the return periods. The first summary row represents the median returns for all 20 historical signals. The next row provides the periodic S&P 500 return data for all dates. In other words, what were the median 1-Week, 2-Week, 1-Month, 2-Month, 3-Month, 6-Month, and 1-Year S&P 500 returns from 1987 to 2014? These values are directly comparable. If an AAII Bull Ratio of over 50%, one week following a 6-month low were bearish, then we would expect the signal performance to be below the performance on "All Days."

The next two rows note the number of up and down observations (out of 20), but the last row is the most meaningful. The last row in the table represents the statistical significance of the returns for each performance period. As noted by SentimenTrader, values above 95% are statistically significant and "the higher the value, the more robust the result."

Figure 1: SentimenTrader 10-22-2014

Intermediate and Long-Term Warning Signal

The red box highlights the S&P performance in the 3 months, 6 months, and 1 year following the research study signal. In every case, the median signal returns for the 20 historical observations were negative. This is highly unusual. As you can see from row two, equity returns have had a significant positive historical return bias, earning returns of 2.5%, 5.3%, and 11.0% for 3-month, 6-month, and 1-year periods respectively.

Contrastingly, the median signal returns for 3-months, 6-months, and 12-months were all negative. The median 6-month and 1-year signal returns were -6.6% and -0.9% respectively, both of which were 11.9% below the "All Days" returns. The "Relevance" or statistical significance levels were 94%, 100%, and 100% for the 3-month, 6-month, and 12-month periods respectively. In other words, the intermediate and long-term study results are highly significant and decidedly bearish.

Conclusion

We should never read too much into any one research study, but we should never ignore statistically significant results either. Economic indicators are not currently consistent with a recessionary environment, but overly euphoric market sentiment only one week after experiencing a 6-month low in the S&P 500 is not encouraging.

Print and Kindle Versions of Brian Johnson's New Book are Now Both Available on Amazon (24 5-Star Reviews)

Trader Edge Strategy E-Subscription Now Available: 20% ROR

The Trader Edge Asset Allocation Rotational (AAR) Strategy is a conservative, long-only, asset allocation strategy that rotates monthly among five large asset classes. The AAR strategy has generated approximately 20% annual returns over the combined back and forward test period (1/1/1990 to 7/29/2013). Please use the above link to learn more about the AAR strategy.

Feedback

Your comments, feedback, and questions are always welcome and appreciated. Please use the comment section at the bottom of this page or send me an email.

Referrals

If you found the information on www.TraderEdge.Net helpful, please pass along the link to your friends and colleagues or share the link with your social network.

The "Share / Save" button below contains links to all major social networks. If you do not see your social network listed, use the down-arrow to access the entire list of social networking sites.

Thank you for your support.

Brian Johnson

Copyright 2014 - Trading Insights, LLC - All Rights Reserved.

Pingback: The Whole Street’s Daily Wrap for 10/30/2014 | The Whole Street