This article presents the Trader Edge aggregate neural network model forecast for the September 2014 non-farm payroll data, which is scheduled to be released tomorrow morning at 8:30 AM EDT.

Non-Farm Payroll (NFP) Model Forecast - September 2014

The Trader Edge aggregate NFP model represents the average of three neural network forecasting models, each of which employs a different neural network architecture. Unlike expert systems, neural networks use algorithms to identify and quantify complex relationships between variables based on historical data. All three models derive their forecasts from seven explanatory variables and the changes in those variables over time.

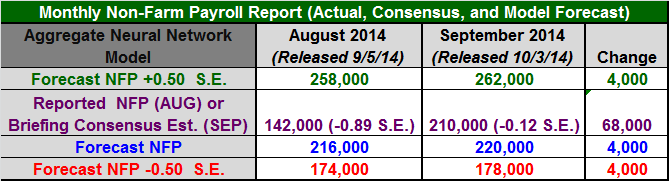

The table in Figure 1 below includes the monthly non-farm payroll data for two months: August and September 2014. The August data was released last month and the non-farm payroll data for September 2014 will be released tomorrow morning at 8:30 AM EDT.

The model forecasts are in the third data row of the table (in blue). Note that past and current forecasts reflect the latest values of the independent variables, which means that forecasts will change when revisions are made to the historical economic data.

The monthly standard error of the model is approximately 83,300 jobs. The first and last data rows of the table report the forecast plus 0.5 standard errors (in green) and the forecast minus 0.5 standard errors (in red), respectively. All values are rounded to the nearest thousand. If the model errors were normally distributed, roughly 31% of the observations would fall below -0.5 standard errors and another 31% of the observations would exceed +0.5 standard errors.

The actual non-farm payroll release for August 2014 is in the second data row of the table (in purple). The consensus estimate (reported by Briefing.com) for September 2014 is also in the second data row of the table (in purple). The reported and consensus NFP values also include the deviation from the forecast NFP (as a multiple of the standard error of the estimate). Finally, the last column of the table includes the estimated changes from August to September 2014.

Figure 1: Non-Farm Payroll Table September 2014

Model Commentary

The aggregate neural network model forecast for September is 220,000, which is up a trivial 4,000 jobs from last month's revised forecast of 216,000. The minimal change in the forecast from August to September reflects a stable employment environment over the past two months. The Briefing.com consensus estimate for September is 210,000, which is up 68,000 jobs from the August report, indicating a strengthening in the employment environment. However, the actual August data was significantly below revised August forecast (-0.89 S.E.), which strongly suggests the actual August NFP data was a one-month outlier. The consensus estimate for September is slightly lower than the model forecast (-0.12 S.E.).

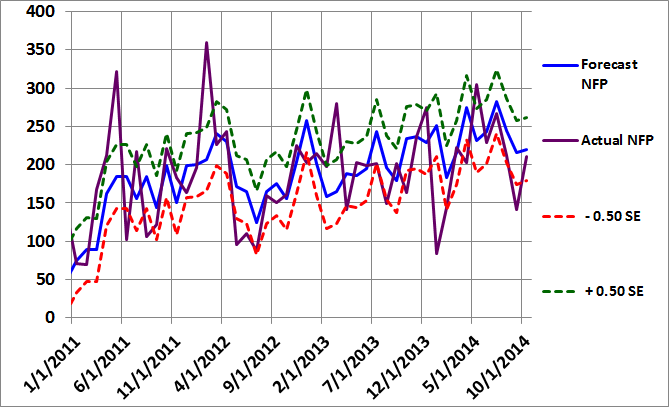

If we ignore the extraordinary outlier in the December data (-2.01 S.E), there had been a gradual and sustained positive trend in the employment data from late 2012 until mid-2014. However, that trend has begun to reverse in the last few months, especially if the August data does not prove to be an isolated outlier.

Not surprisingly, the variation in the actual NFP reports is much wider than the variation in the NFP forecasts. Unfortunately, the Government reports are notoriously noisy, so the trend is more apparent in the forecast data, which are based on several different economic variables that collectively give a much more accurate and reliable employment reading than the Government data.

The minimal difference between the September NFP consensus and September NFP forecast provides little if any insight into the direction of a potential surprise tomorrow. However, it will be interesting to see if the sharp decline in August is reversed in September.

Figure 2: Non-Farm Payroll Graph September 2014

Summary

Basic forecasting tools can help you identify unusual consensus economic estimates, which often lead to substantial surprises and market movements. Identifying such environments in advance may help you protect your portfolio from these corrections and help you determine the optimal entry and exit points for your strategies.

In the case of the NFP data, the monthly report data is highly variable and prone to substantial revisions. As a result, having an independent and unbiased indicator of the health of the U.S. job market is especially important.

Print and Kindle Versions of Brian Johnson's New Book are Now Both Available on Amazon (Twenty 5-Star Reviews)

Option Strategy Risk / Return Ratios: A Revolutionary New Approach to Optimizing, Adjusting, and Trading Any Option Income Strategy

Trader Edge Strategy E-Subscription Now Available: 20% ROR

The Trader Edge Asset Allocation Rotational (AAR) Strategy is a conservative, long-only, asset allocation strategy that rotates monthly among five large asset classes. The AAR strategy has generated 20%+ annual returns over the 20+ year combined back and forward test period. Please use the above link to learn more about the AAR strategy.

Feedback

Your comments, feedback, and questions are always welcome and appreciated. Please use the comment section at the bottom of this page or send me an email.

Referrals

If you found the information on www.TraderEdge.Net helpful, please pass along the link to your friends and colleagues or share the link with your social or professional networks.

The "Share / Save" button below contains links to all major social and professional networks. If you do not see your network listed, use the down-arrow to access the entire list of networking sites.

Thank you for your support.

Brian Johnson

Copyright 2014 - Trading Insights, LLC - All Rights Reserved.

About Brian Johnson

I have been an investment professional for over 30 years. I worked as a fixed income portfolio manager, personally managing over $13 billion in assets for institutional clients. I was also the President of a financial consulting and software development firm, developing artificial intelligence based forecasting and risk management systems for institutional investment managers.

I am now a full-time proprietary trader in options, futures, stocks, and ETFs using both algorithmic and discretionary trading strategies.

In addition to my professional investment experience, I designed and taught courses in financial derivatives for both MBA and undergraduate business programs on a part-time basis for a number of years. I have also written four books on options and derivative strategies.

Non-Farm Payroll (NFP) Model Forecast – September 2014

This article presents the Trader Edge aggregate neural network model forecast for the September 2014 non-farm payroll data, which is scheduled to be released tomorrow morning at 8:30 AM EDT.

Non-Farm Payroll (NFP) Model Forecast - September 2014

The Trader Edge aggregate NFP model represents the average of three neural network forecasting models, each of which employs a different neural network architecture. Unlike expert systems, neural networks use algorithms to identify and quantify complex relationships between variables based on historical data. All three models derive their forecasts from seven explanatory variables and the changes in those variables over time.

The table in Figure 1 below includes the monthly non-farm payroll data for two months: August and September 2014. The August data was released last month and the non-farm payroll data for September 2014 will be released tomorrow morning at 8:30 AM EDT.

The model forecasts are in the third data row of the table (in blue). Note that past and current forecasts reflect the latest values of the independent variables, which means that forecasts will change when revisions are made to the historical economic data.

The monthly standard error of the model is approximately 83,300 jobs. The first and last data rows of the table report the forecast plus 0.5 standard errors (in green) and the forecast minus 0.5 standard errors (in red), respectively. All values are rounded to the nearest thousand. If the model errors were normally distributed, roughly 31% of the observations would fall below -0.5 standard errors and another 31% of the observations would exceed +0.5 standard errors.

The actual non-farm payroll release for August 2014 is in the second data row of the table (in purple). The consensus estimate (reported by Briefing.com) for September 2014 is also in the second data row of the table (in purple). The reported and consensus NFP values also include the deviation from the forecast NFP (as a multiple of the standard error of the estimate). Finally, the last column of the table includes the estimated changes from August to September 2014.

Figure 1: Non-Farm Payroll Table September 2014

Model Commentary

The aggregate neural network model forecast for September is 220,000, which is up a trivial 4,000 jobs from last month's revised forecast of 216,000. The minimal change in the forecast from August to September reflects a stable employment environment over the past two months. The Briefing.com consensus estimate for September is 210,000, which is up 68,000 jobs from the August report, indicating a strengthening in the employment environment. However, the actual August data was significantly below revised August forecast (-0.89 S.E.), which strongly suggests the actual August NFP data was a one-month outlier. The consensus estimate for September is slightly lower than the model forecast (-0.12 S.E.).

If we ignore the extraordinary outlier in the December data (-2.01 S.E), there had been a gradual and sustained positive trend in the employment data from late 2012 until mid-2014. However, that trend has begun to reverse in the last few months, especially if the August data does not prove to be an isolated outlier.

Not surprisingly, the variation in the actual NFP reports is much wider than the variation in the NFP forecasts. Unfortunately, the Government reports are notoriously noisy, so the trend is more apparent in the forecast data, which are based on several different economic variables that collectively give a much more accurate and reliable employment reading than the Government data.

The minimal difference between the September NFP consensus and September NFP forecast provides little if any insight into the direction of a potential surprise tomorrow. However, it will be interesting to see if the sharp decline in August is reversed in September.

Figure 2: Non-Farm Payroll Graph September 2014

Summary

Basic forecasting tools can help you identify unusual consensus economic estimates, which often lead to substantial surprises and market movements. Identifying such environments in advance may help you protect your portfolio from these corrections and help you determine the optimal entry and exit points for your strategies.

In the case of the NFP data, the monthly report data is highly variable and prone to substantial revisions. As a result, having an independent and unbiased indicator of the health of the U.S. job market is especially important.

Print and Kindle Versions of Brian Johnson's New Book are Now Both Available on Amazon (Twenty 5-Star Reviews)

Option Strategy Risk / Return Ratios: A Revolutionary New Approach to Optimizing, Adjusting, and Trading Any Option Income Strategy

Trader Edge Strategy E-Subscription Now Available: 20% ROR

The Trader Edge Asset Allocation Rotational (AAR) Strategy is a conservative, long-only, asset allocation strategy that rotates monthly among five large asset classes. The AAR strategy has generated 20%+ annual returns over the 20+ year combined back and forward test period. Please use the above link to learn more about the AAR strategy.

Feedback

Your comments, feedback, and questions are always welcome and appreciated. Please use the comment section at the bottom of this page or send me an email.

Referrals

If you found the information on www.TraderEdge.Net helpful, please pass along the link to your friends and colleagues or share the link with your social or professional networks.

The "Share / Save" button below contains links to all major social and professional networks. If you do not see your network listed, use the down-arrow to access the entire list of networking sites.

Thank you for your support.

Brian Johnson

Copyright 2014 - Trading Insights, LLC - All Rights Reserved.

About Brian Johnson

I have been an investment professional for over 30 years. I worked as a fixed income portfolio manager, personally managing over $13 billion in assets for institutional clients. I was also the President of a financial consulting and software development firm, developing artificial intelligence based forecasting and risk management systems for institutional investment managers. I am now a full-time proprietary trader in options, futures, stocks, and ETFs using both algorithmic and discretionary trading strategies. In addition to my professional investment experience, I designed and taught courses in financial derivatives for both MBA and undergraduate business programs on a part-time basis for a number of years. I have also written four books on options and derivative strategies.