The following article updates the diffusion index, recession slack index, aggregate recession model, and aggregate peak-trough model through May 2015. In January 2015, I created a new explanatory variable for a market-based indicator and I added another new explanatory variable in April 2015. The total total number of explanatory recession model variables is now 20. The current and historical data in this report reflect the current model configuration with all 20 variables.

In July 2014, two new explanatory variables were added to the Trader Edge Recession Models and one explanatory variable was replaced. The swapped variables measured similar economic data, but the new series had more predictive power and was more forward-looking. For more information on the changes in July 2014, please see "Two New Improvements to Trader Edge Recession Models."

Diffusion Index

The Trader Edge diffusion index equals the percentage of independent variables indicating a recession. With the additions, there are now a total of 20 explanatory variables, each with a unique look-back period and recession threshold. The resulting diffusion index and changes in the diffusion index are used to calculate the probit, logit, and neural network model forecasts.

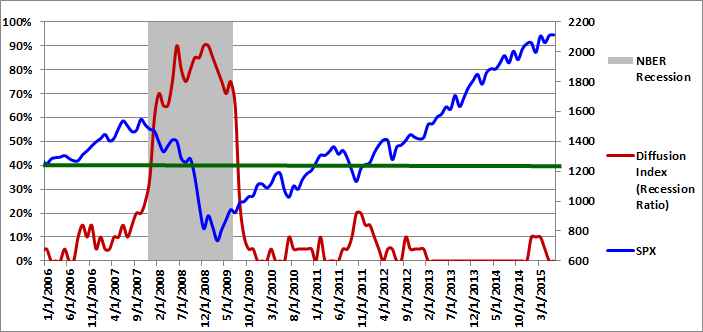

The graph of the diffusion index from 1/1/2006 to 6/1/2015 is presented in Figure 1 below (in red - left axis). If you would like to view a graph of the earlier historical data (going back to 1960), please revisit A New Recession Slack Indicator. The gray shaded regions in Figure 1 below represent U.S. recessions as defined (after the fact) by the National Bureau of Economic Research (NBER). The value of the S&P 500 index is also included (in blue - right axis).

In December 2014, for the first time since late 2011-early 2012, two of the 19 explanatory variables simultaneously indicated a recessionary environment; two variables continued to indicate a recessionary environment in January and February 2015. The number of variables indicating a recession dropped to one in March, and declined again to zero in April, where it remained in May.

In non-recessionary environments, such weakness tends to persist for a few months and then dissipates. However, if the weakness becomes more widespread or lingers for many months, that would be more problematic. The weakness in the diffusion index persisted for several months, but has since declined to zero.

Please note that past estimates and index values will change whenever the historical data is revised. All current and past forecasts and index calculations are based on the latest revised data.

Figure 1: Diffusion Index 06-01-2015

Recession Slack Index

The Trader Edge recession slack index equals the median standardized deviation of the current value of the explanatory variables from their respective recession thresholds. The resulting value signifies the amount of slack or cushion relative to the recession threshold, expressed in terms of the number of standard deviations.

The gray shaded regions in Figure 2 below represent U.S. recessions as defined (after the fact) by the NBER. The median recession slack index is depicted in purple and is plotted against the right axis, which is expressed as the number of standard deviations above the recession threshold.

The dark-red, horizontal line at 0.50 standard deviations denotes a possible warning threshold for the recession slack index. Many of the past recessions began when the recession slack index crossed below 0.50. Similarly, many of the past recessions ended when the recession slack index crossed back above 0.0.

At the end of November 2014, the revised median recession slack index was 1.19, comfortably above the warning level of 0.50. The revised values of the recession slack index declined alarmingly to 0.62 in March, perilously close to the early warning level of 0.50. The value of 0.62 was the lowest value recorded since the end of the Great Recession. The median recession slack index did bounce back to 0.90 in April, but declined again in May to 0.81. The recent decline in the recession slack index is troubling and the cushion above the warning level has shrunk considerably since late-2014.

The ability to track small variations and trend changes over time illustrates the advantage of monitoring the continuous recession slack index in addition to the diffusion index above, which moves in discrete steps.

While it is useful to track the actual recession slack index values directly, the values are also used to generate the more intuitive probit and logit probability forecasts.

Figure 2: Median Recession Slack Index 06-01-2015

Aggregate Recession Probability Estimate

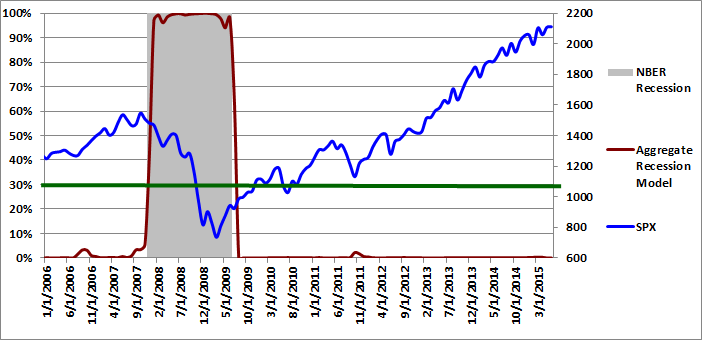

The Trader Edge aggregate recession model is the average of four models: the probit and logit models based on the diffusion index and the probit and logit models based on the recession slack index. The aggregate recession model estimates from 1/1/2006 to 06/01/2015 are depicted in Figure 3 below (red line - left vertical axis). The gray shaded regions represent NBER recessions and the blue line reflects the value of the S&P 500 index (right vertical axis). I suggest using a warning threshold of between 30-40% for the aggregate recession model (green horizontal line).

The aggregate recession model probability estimate for 06/01/2015 was 0.0%, which was unchanged from last month's value of 0.0%. According to the model, the probability that the U.S. is currently in a recession continues to be extremely remote.

Figure 3: Aggregate Recession Model 06-01-2015

Aggregate Peak-Trough Probability Estimate

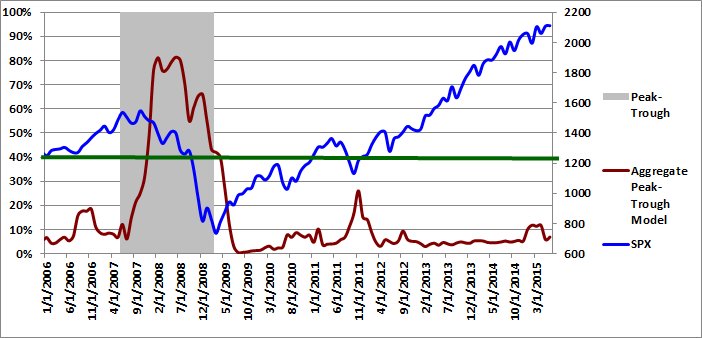

The peak-trough model forecasts are different from the recession model. The peak-trough models estimate the probability of the S&P 500 being between the peak and trough associated with an NBER recession. The S&P 500 typically peaks before recessions begin and bottoms out before recessions end. As a result, it is far more difficult for the peak-trough model to fit this data and the model forecasts have larger errors than the recession model.

The Trader Edge aggregate peak-trough model equals the weighted-average of nine different models: the probit and logit models based on the diffusion index, the probit and logit models based on the recession slack index, and five neural network models.

The aggregate peak-trough model estimates from 1/1/2006 to 06/01/2015 are depicted in Figure 4 below, which uses the same format as Figure 3, except that the shaded regions represent the periods between the peaks and troughs associated with NBER recessions.

The aggregate peak-trough model probability estimate for 06/01/2015 was 6.9%, which is up slightly from the revised value of 5.9% at the end of April. The peak-trough probability reached 11.8% in January and 11.7% in March. The current peak-trough probability estimate of 6.9% is still well below the early warning threshold of 30% to 40%.

Figure 4: Aggregate Peak-Trough Model 06-01-2015

Conclusion

U.S. recession risk remains low, but has increased since late-2014. The diffusion index jumped from zero to two in December, remained at two in January and February, declined to one in March, and returned to zero in April. In March, the recession slack index dropped to its lowest level since the end of the Great Recession (0.62). It rebounded in April to 0.90, but dropped again in May to 0.81. The peak-trough recession probability estimate increased dropped back below double digits in April and May. All of the forecast values are well inside their respective warning thresholds.

Print and Kindle Versions of Brian Johnson's 2nd Book are Available on Amazon

Exploiting Earnings Volatility: An Innovative New Approach to Evaluating, Optimizing, and Trading Option Strategies to Profit from Earnings Announcements.

Print and Kindle Versions of Brian Johnson's 1st Book are Available on Amazon (35 5-Star Reviews)

Option Strategy Risk / Return Ratios: A Revolutionary New Approach to Optimizing, Adjusting, and Trading Any Option Income Strategy

Trader Edge Strategy E-Subscription Now Available: 20% ROR

The Trader Edge Asset Allocation Rotational (AAR) Strategy is a conservative, long-only, asset allocation strategy that rotates monthly among five large asset classes. The AAR strategy has generated annual returns of approximately 20% over the combined back and forward test period. Please use the above link to learn more about the AAR strategy.

Feedback

Your comments, feedback, and questions are always welcome and appreciated. Please use the comment section at the bottom of this page or send me an email.

Referrals

If you found the information on www.TraderEdge.Net helpful, please pass along the link to your friends and colleagues or share the link with your social or professional networks.

The "Share / Save" button below contains links to all major social and professional networks. If you do not see your network listed, use the down-arrow to access the entire list of networking sites.

Thank you for your support.

Brian Johnson

Copyright 2015 - Trading Insights, LLC - All Rights Reserved.

Recession Model Forecast: 06-01-2015

The following article updates the diffusion index, recession slack index, aggregate recession model, and aggregate peak-trough model through May 2015. In January 2015, I created a new explanatory variable for a market-based indicator and I added another new explanatory variable in April 2015. The total total number of explanatory recession model variables is now 20. The current and historical data in this report reflect the current model configuration with all 20 variables.

In July 2014, two new explanatory variables were added to the Trader Edge Recession Models and one explanatory variable was replaced. The swapped variables measured similar economic data, but the new series had more predictive power and was more forward-looking. For more information on the changes in July 2014, please see "Two New Improvements to Trader Edge Recession Models."

Diffusion Index

The Trader Edge diffusion index equals the percentage of independent variables indicating a recession. With the additions, there are now a total of 20 explanatory variables, each with a unique look-back period and recession threshold. The resulting diffusion index and changes in the diffusion index are used to calculate the probit, logit, and neural network model forecasts.

The graph of the diffusion index from 1/1/2006 to 6/1/2015 is presented in Figure 1 below (in red - left axis). If you would like to view a graph of the earlier historical data (going back to 1960), please revisit A New Recession Slack Indicator. The gray shaded regions in Figure 1 below represent U.S. recessions as defined (after the fact) by the National Bureau of Economic Research (NBER). The value of the S&P 500 index is also included (in blue - right axis).

In December 2014, for the first time since late 2011-early 2012, two of the 19 explanatory variables simultaneously indicated a recessionary environment; two variables continued to indicate a recessionary environment in January and February 2015. The number of variables indicating a recession dropped to one in March, and declined again to zero in April, where it remained in May.

In non-recessionary environments, such weakness tends to persist for a few months and then dissipates. However, if the weakness becomes more widespread or lingers for many months, that would be more problematic. The weakness in the diffusion index persisted for several months, but has since declined to zero.

Please note that past estimates and index values will change whenever the historical data is revised. All current and past forecasts and index calculations are based on the latest revised data.

Figure 1: Diffusion Index 06-01-2015

Recession Slack Index

The Trader Edge recession slack index equals the median standardized deviation of the current value of the explanatory variables from their respective recession thresholds. The resulting value signifies the amount of slack or cushion relative to the recession threshold, expressed in terms of the number of standard deviations.

The gray shaded regions in Figure 2 below represent U.S. recessions as defined (after the fact) by the NBER. The median recession slack index is depicted in purple and is plotted against the right axis, which is expressed as the number of standard deviations above the recession threshold.

The dark-red, horizontal line at 0.50 standard deviations denotes a possible warning threshold for the recession slack index. Many of the past recessions began when the recession slack index crossed below 0.50. Similarly, many of the past recessions ended when the recession slack index crossed back above 0.0.

At the end of November 2014, the revised median recession slack index was 1.19, comfortably above the warning level of 0.50. The revised values of the recession slack index declined alarmingly to 0.62 in March, perilously close to the early warning level of 0.50. The value of 0.62 was the lowest value recorded since the end of the Great Recession. The median recession slack index did bounce back to 0.90 in April, but declined again in May to 0.81. The recent decline in the recession slack index is troubling and the cushion above the warning level has shrunk considerably since late-2014.

The ability to track small variations and trend changes over time illustrates the advantage of monitoring the continuous recession slack index in addition to the diffusion index above, which moves in discrete steps.

While it is useful to track the actual recession slack index values directly, the values are also used to generate the more intuitive probit and logit probability forecasts.

Figure 2: Median Recession Slack Index 06-01-2015

Aggregate Recession Probability Estimate

The Trader Edge aggregate recession model is the average of four models: the probit and logit models based on the diffusion index and the probit and logit models based on the recession slack index. The aggregate recession model estimates from 1/1/2006 to 06/01/2015 are depicted in Figure 3 below (red line - left vertical axis). The gray shaded regions represent NBER recessions and the blue line reflects the value of the S&P 500 index (right vertical axis). I suggest using a warning threshold of between 30-40% for the aggregate recession model (green horizontal line).

The aggregate recession model probability estimate for 06/01/2015 was 0.0%, which was unchanged from last month's value of 0.0%. According to the model, the probability that the U.S. is currently in a recession continues to be extremely remote.

Figure 3: Aggregate Recession Model 06-01-2015

Aggregate Peak-Trough Probability Estimate

The peak-trough model forecasts are different from the recession model. The peak-trough models estimate the probability of the S&P 500 being between the peak and trough associated with an NBER recession. The S&P 500 typically peaks before recessions begin and bottoms out before recessions end. As a result, it is far more difficult for the peak-trough model to fit this data and the model forecasts have larger errors than the recession model.

The Trader Edge aggregate peak-trough model equals the weighted-average of nine different models: the probit and logit models based on the diffusion index, the probit and logit models based on the recession slack index, and five neural network models.

The aggregate peak-trough model estimates from 1/1/2006 to 06/01/2015 are depicted in Figure 4 below, which uses the same format as Figure 3, except that the shaded regions represent the periods between the peaks and troughs associated with NBER recessions.

The aggregate peak-trough model probability estimate for 06/01/2015 was 6.9%, which is up slightly from the revised value of 5.9% at the end of April. The peak-trough probability reached 11.8% in January and 11.7% in March. The current peak-trough probability estimate of 6.9% is still well below the early warning threshold of 30% to 40%.

Figure 4: Aggregate Peak-Trough Model 06-01-2015

Conclusion

U.S. recession risk remains low, but has increased since late-2014. The diffusion index jumped from zero to two in December, remained at two in January and February, declined to one in March, and returned to zero in April. In March, the recession slack index dropped to its lowest level since the end of the Great Recession (0.62). It rebounded in April to 0.90, but dropped again in May to 0.81. The peak-trough recession probability estimate increased dropped back below double digits in April and May. All of the forecast values are well inside their respective warning thresholds.

Print and Kindle Versions of Brian Johnson's 2nd Book are Available on Amazon

Exploiting Earnings Volatility: An Innovative New Approach to Evaluating, Optimizing, and Trading Option Strategies to Profit from Earnings Announcements.

Print and Kindle Versions of Brian Johnson's 1st Book are Available on Amazon (35 5-Star Reviews)

Option Strategy Risk / Return Ratios: A Revolutionary New Approach to Optimizing, Adjusting, and Trading Any Option Income Strategy

Trader Edge Strategy E-Subscription Now Available: 20% ROR

The Trader Edge Asset Allocation Rotational (AAR) Strategy is a conservative, long-only, asset allocation strategy that rotates monthly among five large asset classes. The AAR strategy has generated annual returns of approximately 20% over the combined back and forward test period. Please use the above link to learn more about the AAR strategy.

Feedback

Your comments, feedback, and questions are always welcome and appreciated. Please use the comment section at the bottom of this page or send me an email.

Referrals

If you found the information on www.TraderEdge.Net helpful, please pass along the link to your friends and colleagues or share the link with your social or professional networks.

The "Share / Save" button below contains links to all major social and professional networks. If you do not see your network listed, use the down-arrow to access the entire list of networking sites.

Thank you for your support.

Brian Johnson

Copyright 2015 - Trading Insights, LLC - All Rights Reserved.

About Brian Johnson

I have been an investment professional for over 30 years. I worked as a fixed income portfolio manager, personally managing over $13 billion in assets for institutional clients. I was also the President of a financial consulting and software development firm, developing artificial intelligence based forecasting and risk management systems for institutional investment managers. I am now a full-time proprietary trader in options, futures, stocks, and ETFs using both algorithmic and discretionary trading strategies. In addition to my professional investment experience, I designed and taught courses in financial derivatives for both MBA and undergraduate business programs on a part-time basis for a number of years. I have also written four books on options and derivative strategies.